Sometimes corporations find it helpful to restructure their debt.

In times of lower interest rates corporations may call in older issued debt.

They will refund the borrowers, and they may issue new debt at the lower

interest rate. This process is called refunding.

The first three items on this list is the $126 billion of

long-term debt that the treasury has announced the auction of this week.

The last four items amount to $165 billion of

shorter-term debt set for auction this week. Each item includes

the auction date and the issuance date. On the auction day

auction participants may hedge their bid by placing a trade on the open market.

After issuance the securities will be available for direct selling on the market.

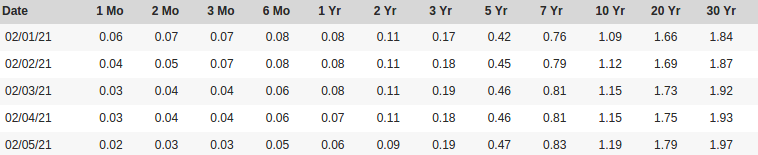

The Yield Curve

One of the confusing things about interest rates is that there are so many

different types of interest rates. Even when only talking about government

debt, there is a whole curve of interest rates to report. The government

generally pays more interest on loans for a longer period of time. This table

shows the yield curve for five recent days as reported by the treasury.

These data show a clear trend. Treasury yields for periods of 2 years or less

have been falling. Treasury yields for periods of 3 years or more are rising.

The current refunding of the treasury was done to replace shorter term loans

with longer term loans. A reduction of the supply of shorter term bills could

explain a reduction in short-term yields.

The recent changes in treasury yields may reflect a pricing in of the expected

auction next week. It's also possible that the auction is not fully priced in

and the trend will continue.

In grad school, I attended a few seminars on the topic of game theory. I

lament that, at that time, I did not accept game theory as a serious discipline.

With the passage of time, I've come to realize that the principles that define

game theory are evidenced everywhere. For example, one could argue that the

study of economics is a study of game theory. Game theory applies to markets.

Game theory applies to politics. You may remember John Nash applying game theory

to suiting—human mating—in the movie A Beautiful Mind.

I was in an audience where David Friedman explained a fundamental flaw in

political democracy: any random voter has very little motivation to research any

potential outcome governed by democratic process. Most likely, one individual

vote will not have any influence on the outcome of an election. Imagine if you

spent a great deal of time researching potential presidential hopefuls for the

2024 election and identified Sarah Harberter from Indiana as the perfect

candidate. Imagine backing up this research with a 500-page, well-cited report.

How would you reap the rewards of your research? Where is the incentive? All

apologies to anyone named Sarah Harberter. The name is fictional and introduced

soley for the purposes of this article.

Publicly-traded companies make decisions via a different flavor of democracy. In

a shareholder meeting, investors who have a larger stake in the company, will

exercise more influence over the outcome of those decisions. This incentive may

encourage, for example, a 10% shareholder to hire people to perform independent

research before a decision is made. Though there is some alignment of

incentives—both the company and the investors want to make money—it may be in

the company's best interest to sometimes deceive those investors. Investors know

of this potentiality and will often perform necessary due diligence to avoid

deception. Incentives.

A particularly influential aspect of my personal and professional life has been

affected by this second type of voting—the type of voting where the people most

impacted by a decision have the most say. But these votes are not the votes of

shareholders. These votes reflect the desire of the Dash network manifested as a

Decentralized Autonomous Organization or DAO (more on the DAO later). This DAO

elected me to be one of the supervisors for the Dash Investment Foundation or

DIF. And that committee of supervisors elected me to be their chair. These are

the votes that matter most in my life.

Governance

Governance is a neat word and fascinating concept. Merriam-Webster defines

governance as "the act or process of governing or overseeing the control and

direction of something." I govern my body. Your household governs your home,

family, and finances. Corporate charters and by-laws and shareholders govern

companies. Well-functioning governance can be elegant and provide great value.

In the past, I have given talks where I assert the most important gift that

Satoshi Nakamoto granted the world was a robust and well-defined form of

governance for a specific use case—cryptocurrency. Nakamoto's software includes

all the rules that govern what makes money, money, baked-in up front. But that

set of rules, though interesting and necessary, isn't the innovative element of

the design. The bigger deal is that the software enforces these rules upon

itself and the network—software governing software in the wild. Rouge

software trying to spoof the network is automatically detected and ignored.

Nakamoto designed a computer network that both

derives its governance from and

enforces its governance on the network.

Many physicists think that the universe arose from a singularity. I'm trying to

describe a singularity that results from governance.

Enter Dash

The Dash project (dash, as in digital cash) implemented a unique approach to

this design that seems to have best leveraged and extended this governance

model. A first governance change served to promote, through financial incentive,

deployment of a more robust, network-servicing infrastructure. Bitcoin provides

an incentive for deploying compute-power in the form of mining only. Dash

provides incentives that encourage compute-power for additional and augmenting

tasks needed by the network. We call these compute resources masternodes. A

second governance change enabled the masternode operators to allocate (through a

vote) a designated portion of network-generated funds to proposed projects that

target improvement or strengthening of the Dash project, network, and protocol.

This aspect to the governance model is called a Decentralized Autonomous

Organization, or DAO.

Dash Core Group is one company that has had consistent funding from the

network. Dash Core Group shepherds the development, maintenance, and enhancement

of the core software that makes the network possible. This augmentation to the

governance model (the DAO) was the first step towards extending the protocol's

governance beyond the hardware. The Dash network, through a decentralized

decision-making process, is enabled to fund or not fund any project or

organization.

The formation of the Dash Investment Foundation (the DIF) was another milestone

illustrating the power of this governance model. This foundation operates in the

real world, acting as a legal entity in the same way any other corporation does.

The foundation is only in its second year of operation but has recently gone

under contract to enable the Dash network to receive equity in ReadyRaider, an

esports platform that exclusively accepts dash. So the governance cascade

continues. With the foundation, the Dash network governs a corporation. A

corporation that can then partner with other entities in ways that are

ultimately governed by the network.

It's been a long road, but if you will allow me a bit of tongue-in-cheek:

governance led to governance that led to infrastructure that plugs into the

legal system of governance of governments. I can't adequately express the

excitement and wonder that this imparts on me. Nerds, governed by governments,

made a governance that did not need a government which can now govern an entity

that is recognized by governments. Excuse me if I may be a bit emphatic: shit

just got real.

Oddly, there have been several occasions when markets reacted as if they had a

better understanding of events than should have been possible. This happens

often enough that it's difficult to blame these phenomena solely on insider

trading.

When witness to the results of a Dash Network voting cycle, I have often been

perplexed about the decisions made by the masternodes. I have been surprised to

see existing valuable infrastructure defunded, for example. However, I believe

these decisions have been ultimately proven wise as time unfolds. It is easy to

be upset about withheld or terminated funding. But it is also difficult to

identify the opportunities made available by those freed resources. If I had to

judge the Dash DAO as an entity by the decisions that it has made, I would judge

this entity to be wise. I lament that the DAO cannot manifest and explain its

reasoning.

I believe there is wisdom behind the decision of the DAO not to fund recent DIF

proposals. I believe the DAO has identified how interests have gotten

out-of-whack. Muddled. I believe the DAO is holding out until the DIF can

demonstrate a more efficient use of resources. I believe this so strongly, that

I am putting my time where my mouth is by becoming a DIF protector.

A Conflict of Interest

Let us consider a masternode owner, Alice. Alice pays $20 a month for access to

a server where she runs the software required to service the Dash Network.

Alice's node serves the network and is placed on the rewards queue. Alice waits

patiently as every other node is called before hers, and then her number comes

up and she receives 1.44236253 DASH and fees as a payment. Alice faithfully

researches proposals every cycle and offers up her vote.

Alice then notices that there is a proposal for the DIF that would fund a

masternode run by the DIF. Alice understands that another masternode would

incrementally lengthen the line at the payment queue. Alice also understands

that if the DIF runs masternodes then her veto as part of the DAO will be

similarly diluted. For these reasons alone Alice might not vote to fund the

DIF.

A DIF that seeks funding from the DAO for the purpose of running masternodes,

even if run through a third party, will always make their proposals

incrementally less attractive. Such a DIF is a competitor to masternode owners,

like Alice. Despite the fact that the DIF is supposedly working hand-in-hand

with the DAO, we may even go as far to say that such a DIF is instead marginally

adversarial to Alice and therefore even the DAO.

Trolls on the Internet

Having been around for a while I see some people on the internet argue that Dash

Core Group (DCG) should not run masternodes. This is a straw man argument since

DCG does not run masternodes. However, the same conflict of interest would

apply if they did.

There are those that misrepresent facts and extend this line of reasoning,

arguing that contractors paid by DCG should not run masternodes. That argument

simply doesn't follow though. People who have an interest in a masternode are

naturally going to be incented to do beneficial work for DCG. As long as the

payment is representative of the value provided, there simply is no conflict of

interest. This argument gets even weaker when it is considered that some working

for DCG are working for no, or reduced pay (note that we hope this situation

will improve in months to come).

More than Money

Money is meaningless if it doesn't buy anything. I would expect the DIF to hedge

in order to protect wealth. Running a masternode sets up a game theoretic

situation that is not conducive to cooperation. I hope the DIF can convert

money into assets that add value instead of using money to dilute the value of

running a masternode.

This post presents a proposed adjustment and clarification of the prioritized

goals of the Dash Investment Foundation (DIF) and how to measure the successful

achievement of those goals. As with any project, goals and success criteria need

to be well articulated and agreed upon.

In my view, the DIF should pursue two main goals, each aligned to the two types of investment the DIF engages in.

Venture Capital: Provide a process and a legal framework that will

allow the network to fund for-profit ventures in exchange for equity.

Assets Under Management: Generally increase assets under management.

I consider these goals to be listed in the optimal order of priority. The first

goal is directly based on the announcement introducing the Dash Investment

Foundation.

The Dash Investment Foundation enables the Dash treasury to serve as a source of

venture capital and not just as a provider of grants for work on the network and

projects. In this article, I outline how I expect that process to work.

A discussion of Assets Under Management will be reserved for a separate post.

Clarifying Terms

In the world of investing, an association of people may pool resources. We can

call this association of people a fund, effectively. And as with most funds,

they will likely choose to focus on a targeted type of investment.

Private Equity

It might be the case that the fund is established to invest in new companies

(startups). Such a fund is called a venture fund or a private equity fund

and the money raised by a startup is called venture capital. A share in the

ownership of the company is called private equity and is exchanged for those

venture capital funds.

Public equity in the form of common stock is similar in concept but comes

with fewer ownership privileges and is exchanged on the open market at a stock

exchange. A private company does not offer public ownership shares. A public

company offers both. Startups begin as private entities funded by private equity

funds and angel investors.

Angel investors are individuals who stake their own money in a startup in the

form of a private equity investment.

Hedging

A fund could also be established that actively trades in the market with the

goal of making money. Perhaps the first rule of making money is not losing money.

One way to avoid losing money is by hedging. Consider this: Maybe we know that

there is a 60% chance of a particular asset appreciating. We might be able to

bet on the asset going up in price but at the same time hedge. To

hedge would be to make a

contrary bet that will make the downside less likely or have less severe of an

impact. This is difficult to describe in a couple sentences, but the 60% chance

of asset price appreciation could mean the hedged position has an 80% chance of

returning a profit. One way we can help ensure a fund makes money with more

consistency is to hedge.

A fund of this nature is called a hedge fund. The name helps guide the operation

of the fund. This more consistent and increased chance of profit comes with a

cost. An increased chance of a profit generally means that the profit will be

less than if the position was not hedged.

Investing Approach

Private Equity

I interviewed a successful angel investor who warned me that only about 10% of

startups are successful. A few implications of this statement:

An angel would need to invest in 10 startups until they could reasonably

expect a return.

Even if an angel invests in ten startups, there is still a 34% chance that all

startups will have no return.

In order for an angel to be profitable, they must select investments with a

return which is generally greater than 10 fold.

Let that sink in for a moment.

Professionals who invest in private equity fund a tremendous number of projects

that never provide any return. What chance can an amateur have? In a sense,

the DIF can also be viewed as a startup which categorizes the DIF in this same

class of entities that fail 90% of the time.

Hedge Fund

The skills needed to establish a successful hedge fund diverge substantially

from those needed to establish a private equity fund. Hedge funds will often hire people who are particularly

good at math. Such people are called quants, short for quantitative

analysts. My gym buddy in grad school, Ganesh, became a quant. The type of math

used by a hedge fund might depend on the particular specialty of the fund.

Here's a video of my favorite fictional quant: Peter Sullivan from the movie

Margin Call. Be aware, there is cursing in this video.

The DIF in Context

From my assessment, for the past year, the DIF has taken on the role of a both a

venture capital firm and a hedge fund. Attempting to tackle both roles dramatically increases

the amount of mental effort needed. It also requires a much broader set of

skills compared to what is needed for just one of these endeavors. I do see an

opportunity for the DIF to take on both roles. However, for the purposes of this

article I will only discuss the venture capital side of the house.

In his original vision for the DIF, Ryan Taylor identified a missed

opportunity—correctly, in my view—involving the Dash DAO (Decentralized

Autonomous Organization). Traditionally, the Dash DAO has no means to invest and

only a means to issue grants. Ryan noted that the network at times funded

for-profit ventures, but, since the only tool available was a grant, there was

never an exchange of equity in return. And in other cases, companies that would

have potentially benefited the network's infrastructure (an oblique dividend)

were passed over because DAO voters were hesitant to issue a grant to a private

business. To voters, there was often no direct and obvious benefit to anyone but

the business itself.

The DIF was created to address this with an alternative model of funding. The

DIF allows for a level of flexibility in contrast to the rigidity of the Dash

DAO. Scenarios that benefit the Dash Network by empowering a for-profit entity

through funding are made more attractive by offering equity in exchange.

A More Productive, More Manageable Workload for the DIF

Traditionally, startups seek out their own funding. A venture fund that instead

goes looking for startups is much more likely to find poorer quality projects.

Therefore, the Dash DAO and DIF should avoid seeking startups for investment.

Startups should instead seek out the DAO for funding. The DIF would then serve

as the point of contact and facilitator for startups who want to conduct

business with the Dash DAO.

Once contact has been made, a startup would approach the DIF and offer a certain

amount of equity for some value of DASH. For example, "ACME Startup is prepared

to offer a 10% stake in our company in exchange for 120 DASH." At that point,

the DIF would be expected to begin an investigation into the business,

establishing:

The startup does not break any laws.

The startup is generally moral and ethical.

The startup has an appropriate legal structure that will allow a claim of equity to be enforced by a reasonable jurisdiction.

The DIF and the Dash DAO have no conflict of interest by accepting equity.

The startup has a business plan that is clear to understand.

The startup is willing to disclose financial information such as balance sheets and cash flow statements.

This is a sampling.

With this information in hand, the DIF will be in an informed position to form

an opinion about the startup and the value of the proposal.

A simple example: ACME Startup seeks a 120 DASH investment

For our example, maybe ACME Startup satisfies all of the requirements, but the

DIF feels the offer is simply too expensive. The DIF begins negotiations. The

DIF counteroffers with, "We really like your proposal, but we would feel more

comfortable if you offered 20% equity for 120 DASH." To which ACME responds,

"We'll change our offer to 15% equity in exchange for 120 DASH." In our example,

the DIF deems that fair and agrees.

Negotiations over, ACME Startup submits a proposal to the network and asks for

125 DASH (the extra 5 to recover the 5 DASH proposal fee) in exchange for an 15%

stake in the company. A representative of the DIF should then state the DIFs

opinion. For example, "The DIF Feels that ACME startup contributes meaningfully

to the Dash ecosystem. We find 15% equity acceptable and consider the price

fair."

The DIF will offer similar guidance for each proposed project:

We'll accept the equity but the price is too high.

We feel that due to the nature of the business, it would be harmful to accept equity and we will refuse it.

We were not informed about this project and are unable to accept equity.

A well-executed negotiation before submission to the network should result in

the startup and the DIF speaking with a unified voice. It will also allow

some due diligence to be communicated by the DIF.

Note: masternode owners are still expected to do their own due diligence.

Even if negotiations were unsuccessful, the result is still a proposal

process with far more clarity. Let's say, for example, ACME Startup offered 5%

equity in exchange for 120 DASH, but the DIF stood firm on a 20% stake as being the

fair market value. ACME could still make their proposal. The DIF would then be

in a position to deliver an informed response.

Perhaps, they would not attempt to block the proposal from passing, while still

accepting the equity. The statement in that case might go something like, "We

don't feel the valuation is fair to the DAO, but we will accept the equity." And

perhaps ACME would respond with, "The valuation is fair because blah, blah,

blah." Positions are articulated and the masternodes (who direct the DIF) are

then free to decide, but from a more informed position.

This is a process that can be implemented today. There is no need to wait for an

investment adviser (though the Dash DAO could benefit from having an investment

adviser).

Measurement of Success

In this section I'll outline a minimal condition for success for the DIF. Please

understand that great care has been taken to maximize the value provided to all

players, including the DAO. This is simply game theory, my dear Watson.

I propose the DIF—for the year from August 2020 to July 2021—will be deemed

successful if,

A proposal (or proposals) is passed by the network resulting in equity

received by the DIF, which is then is sold to angel investors for $50,000 or

greater.

If this modest success condition is met, all the "profit" to the network would

be intangible, that is, without a clear valuation (a benefited network by

DAO-enabled company). The DAO has money. More money is nice, but the money has

meaning only when the money provides a good or service that is valuable. If

this success condition is met then the DAO would have funded a company that will

enhance Dash Network's infrastructure. At the same time, the DAO will own a

successful incubator or partner with an angel who maintains the investment while

cycling funds back to the DIF so the cycle can continue.

Why Angels?

Angels not only provide money to startups, angels also provide guidance,

connections, and networking. An angel offers these services with the goal of

positioning their investment, the startup, for success, which, at some point, an

angel hopes to sell for a profit.

The DIF does not have the skills that angels do. Additionally, angels

specialize. They each have very specialized skills and only fund ventures that

fall with the limits of their skillset. Currently, there is no way that the DIF

can be as attractive of a business partner as a self-selected angel.

Generally, if the DIF partners with angels that can support DAO-funded ventures,

that is a value-add for those ventures. But this relationship would also enhance

the funding and facilitation services the DIF provides. Additionally, as the

relationshp with angels and the angel community strengthens and expands, the

value the DIF brings to the network should compound.

Selling to angels helps close the loop. Without angels, the process

is . . .

DAO invests 500 DASH on a startup.

The DIF holds the equity for two, five, or ten years before the equity pays

out, if ever.

Instead, with angels (the price of DASH is $100 for this example), the process

becomes . . .

DAO spends 500 DASH.

The equity is sold for $50,000 within three months and the $50,000 is ready to

go back to work for the network.

Synergies

Synergy is a stupid buzz word, but synergies do exist.

Partnering with angels opens the door to multi-party deals. Perhaps two angels

and the DAO go in together on a venture. Maybe an angel funds a venture and a

proposal is never brought to the DAO; the DIF in that case serving only as

matchmaker. Heck, the DIF could still provide value to the network without even

putting a proposal in front of the DAO. This opens up many opportunities for the

network.

I hope this post adequately articulates what I'm proposing and the flexibility

it brings to the network.

At a 2002 conference: Claudia Miller, Darren Tapp, Uli Walther

My Advisor

My thesis advisor was Uli Walther. During my first few years at Purdue, I passed by his door every day in route to my seventh floor office. I was always very curious and often stopped in to ask Uli a math question. Uli was very patient and gave very detailed answers, often with involved references.

I also appreciated him on a personal level. I enjoyed listening to his soccer stories, but I also appreciated the wisdom he shared. Our relationship grew and I felt comfortable engaging in even more personal discussions, for example, asking him as an East German, about communism. Part of what made him unique was this cultural background. He would tell a funny story and end it with a wide smile. But then other students would be confused because he would often tell a joke with a poker-straight face: in his culture no one thought to laugh at a joke a second time.

Our discussions grew, often spilling over into lunch at the Student Union or off campus. Uli even ventured out with us grad students from time to time to play poker. We used to play a game called Fibonacci Crisscross which, if I remember correctly, he invented. But he was still my advisor and treated that relationship professionally. He would not hold back on constructive criticism. For example, he would often confront me about my poor writing. I will always remember when he explained that "x=2" is a complete sentence: 'x' the subject; '=', a stand in for 'is equal to', serves as the predicate or verb; and '2', naturally, is the object. This was revelatory to me, at the time.

My Study

Uli was a good teacher even though I was his first student. Early on, after I officially became his student, he challenged me with what we called a baby question, or a problem to serve as a warmup to a larger, more significant, PhD-worthy problem. The idea was to tackle a particular problem in two dimensions (simpler) and then progress from there. I also used software to guide me. Unfortunately, Saito published a paper demonstrating the higher-dimensional case. Saito doesn't know it, but I felt like he was picking on me in Indiana all the way from Japan. My work did not assume a reduction the same way he did. That missed case became a chapter in my thesis.

Work on that baby problem morphed into a different study. I wanted to calculate an eigenspace decomposition of a monodromy operator. I tried to prove that this monodromy behaved in a certain manner, only to have Uli state that I was in error. Frustrated, I spent the next day or two trying to prove that I was right. When I presented what I learned to Uli, he swatted down my claim with a very simple counter example.

Now, in a proof, if a counter example can be provided for any statement, that statement must be, by definition, false. For my version of the statement to be true, one of the numbers had to be an eight, whereas Uli trivially demonstrated that it was in fact three. Uli's counter example was so obvious there was no disputing it.

For awhile, I obsessed over this problem and would catch myself trying to prove the same statement over and over again. But then, to bring me back to Earth, I would grab Uli's example and reexamine it. I did this to squelch this obsession and to focus on something more productive. Even in the field of mathematics, we become emotionally attached to old work. But in order to grow and progress, I have had to learn to shove old work aside so I could discover even more beautiful patterns around me.

My Success

So with practice I broke this obsessive pattern of behavior and stopped trying to prove statements I knew to be wrong. Instead I took the advice of my advisor: I began all work with simpler example patterns. That was the lesson that stuck with me after that event. Start with the baby problem, then move forward towards more complexity, towards the actual problem you are attempting to solve.

Lesson learned. I tackled my next problem starting from simpler principles. And with this problem, I couldn't shortcut the answer using a computer. I buckled down and worked out a few simpler examples, which led to tackling harder examples . . . eventually, I saw it: a new pattern emerged.

The next day, I presented the pattern to my advisor. He had only one question: "Can you prove it?" Two weeks later I came back to him and answered with a confident "Yes!" Now, one must understand, as part of the process for laying claim to a discovery, one has to search through the literature and find out if someone else has already proven it. At the time, this task was daunting, but I combed through the research. Eventually, I found some papers where my discovery actually served to augment previous work. I.e., it was additive. In a topology paper, I found another part of my proof similarly addressed, therefore lending validation at least to that part of the problem I was trying to solve. But as I spent the time pouring over prior work, I gradually felt satisfied that my work was indeed new.

But I was in a quandary about the topology result. It was if they solved that part of my proof similarly, but using a completely different language. I could cite the work, but the translation needed to demonstrate how their work confirmed mine proved to be too much. So I included my own algebraic proof while at the same time citing the topology paper. Uli noticed, challenged me on it, but ultimately accepted my approach. The end result: my PhD Thesis, Bernstein-Sato polynomials and Picard-Lefschetz monodromy.

The Lesson

So, the takeaway:

Sometimes figuring out what not to do is more important than what you decide to do.

Today, I sometimes find I still don't heed this lesson. Or at least not often enough. A digression, but several aspects of my life right now are, in fact, reminding me of this lesson.

I hope you have enjoyed this story. I enjoyed writing it and hope to gain by revisiting it. I hope you can too. What a joy it is that we live in an age that this story can be shared with anyone.

This week, I successfully installed GrapheneOS on a brand new Pixel 3a: I now

have a phone run entirely with an open-source operating system. Open source

means the software that runs the phone is available for anyone to inspect,

improve, and repair. By extension, because the code is always open to scrutiny,

and because improvements can be implemented and proposed by anyone, security

vulnerabilities are more likely to be discovered and squashed in a timely

fashion. This means that exploitation by a hacker is far less likely—for

example, a hacker gaining control of the phone's camera, microphone, virtual

keyboard, or network stack.

Additionally, open source means improved security simply by removing tools

that corporations use for data collection. Tools that a hacker undoubtedly knows

how to use far better than you do.

Before Installation

My end goal upon completion of this process was a working and reliable device

that could serve as my primary cell phone. Therefore, I first needed to find a

quality implementation guide; and then I needed to settle on a well-understood,

well-tested phone. In this process, I discovered the GrapheneOS—essentially the

Android operating system with all the proprietary Google bits removed.

GrapheneOS currently supports Pixel 3 phones, which narrowed the selection.

(Pixel 2 phones are also supported, and an experimental version of GraphenOS

exists for Pixel 4.) I settled on a Pixel 3a to minimize complications. It also

had to be unlocked, as some phones made by wireless carriers lock down their

phones so that they can't be used with other companies or operating systems.

A modern smartphone is far more than just the operating system, of course. Apps

for a GrapheneOS phone can be obtained through the F-Droid catalog. All apps

in the F-Droid catalog are open source. From F-Droid one can install the

Aurora Store. Ironically, the Aurora Store is an application that serves to enable

browsing and installation from the Google Play store. Fair warning: it is

unclear whether this application violates Google's Terms of Service.

It is also important to know what to expect before installing GrapheneOS. A

phone running nothing but open-source software won't necessarily be able to

solve every problem. Since GrapheneOS does not include any Google services, apps

that normally rely on those services might not work correctly or not work at

all. For example, Signal messenger normally requires Google push

notifications. As a workaround, Signal on GrapheneOS employs a non-Google

background notification service.

The Installation

I found the GrapheneOS for Pixel 3a installation guide provided by Tales from the Crypt to be quite good. The only hiccup I

ran into was verification of the digital signature for the downloaded GrapheneOS

package. Note, verifying the signature is optional but strongly recommended.

Verifying the signature is the best way to check whether you have the version of

the software intended and that it was not tampered with.

The result is a working phone that I'm very happy with that is run by nothing

but open-source software. I installed my existing Verizon SIM card and the phone

worked right away. As time goes on, I'm sure I'll learn more about what works

and what doesn't, but allow me to provide some initial impressions.

So far, I've identified two apps that don't work on this phone:

Bloomberg: Market & Financial News

Audius Music

Some apps and services actually seem to preform better:

Spotify seems to preform at least as good as I expect.

Sonos works much better than I remember.

My bluetooth earbuds work very well.

The hot spot works very well.

Note, the better performance could be explained by the fact that this phone is

much newer than my old phone.

A core strength of the GraphenOS platform is the F-Droid ecosystem. As mentioned

earlier, F-Droid is a catalog of open-source software that makes software

installation and management simple. The catalog is installed by browsing to the

F-Droid website, downloading the catalog application, and installing it on your

phone. This bootstrapping process, was not difficult. Once you have the F-Droid

catalog installed, installation of available applications is as easy is using

the Google Play store on a typical Android phone.

Some of the applications I installed included andOTP to replace Google

Authenticator, Open Keychain for PGP key management (nice to see an encryption

application so prominent), and calculatorpp which has all the calculator

functions I need. I also installed a terminal emulator and through that

installed Python, the programming language interpreter. I installed SSH and then

remotely explored (from the phone) some of my running computers. I'm sure I

could do this with a stock android phone, but I have never considered them

secure enough.

GrapheneOS requires some technical effort to install and therefore is not for

everyone, but so far I'm quite happy with it. I have no doubt I'll use a

closed-source device from time to time, but who knows, GrapheneOS (and the

robust communities surrounding it and the F-Droid ecosystem) encourages the

notion that an open-source alternative will always be available and improving

well into the future.

The context of this article is the United States economy. The ideas presented

should apply to other countries as well, but I will limit the scope to the US

for the sake of clarity.

Modern Economics

The work of John Maynard Keynes strongly influences economic thinking within

governmental circles. Keynesian theory advocates active, centralized management

of the economy, in particular during times of looming recession. As an economy

dips towards recession, for example, central planners prescribe increased

government spending—the thinking: government spending provides jobs, which

increases spending by people newly flush with money, which in turn employs more

people, which increases spending by people flush with money, . . . rinse;

repeat.

Similarly, when the economy is operating outside of the extremes, central

planners nudge the trajectory of the economy by manipulating interest rates:

increased to prevent excessive growth and burnout; decreased to stimulate

investment and growth.

The Actors

The credit markets comprise many actors, each with different driving

motivations. Two major actors are

The Federal Reserve — the central bank of the United States

The United State Treasury — the entity that receives collected taxes and

manages, as directed by Congress, the national debt

The Federal Reserve manipulates interest rates with two principal objectives:

Maximum employment

Stable prices — via an approximate 2% annual inflation rate target

So far, we have introduced the concept of interest rates without definition.

A variety of interest rate types exist, but for our purposes, in the following

sections, we'll discuss three: Treasury interest rates, the federal funds rate,

and corporate interest rates.

Treasury Interest Rates

When the Treasury wants to borrow money, they may issue a Treasury bond. A

Treasury bond is simply a promise by the Treasury to pay a set amount of money

to the bondholder—say, for example, $10,000—at some set time in the future.

Since we value money in hand today more than promised money in the future, these

bonds sell for less than their $10,000 face value. One can interpret this price

difference as an effective interest rate. Confusingly, the price of a bond

fluctuates. If the price goes up, the effective interest rate goes down, and

vice versa.

Now, not all Treasury bonds pay the same interest rate. The payout period of a

Treasury bond can vary between one month and 30 years. Interest rates on later

maturing treasuries are generally higher than shorter terms. How Treasury yields

change according to maturity term is called the yield curve.

Federal Funds Rate

The federal funds rate is an interest rate set by the Federal Reserve that banks

use to lend to each other overnight. In some respects, this is the most

significant interest rate since it sets a baseline, or a rate floor, for other

short term lending rates. As of this writing, the federal funds rate is 0.1%.

Short term treasuries often earn interest at rates at or approaching the federal

funds rate. Market forces generally ensure this relationship.

Corporate Interest Rates

As governments issue bonds, so too can corporations. While the risk associated

with treasury bonds is considered negligible (no risk of default), corporations

can go bankrupt and fail to honor the full amount of their loans. The market

puts a premium on risk. Corporate bonds come with increased risk; therefore,

investors will require a higher interest rate than offered by the near zero-risk

treasury bonds.

Corporate bonds are each graded for risk of default. Therefore, interest rates

can vary widely from company to company, bond to bond. Corporate bonds allow

companies to secure loans without a bank by enabling professional or everyday

investors to fund companies directly, and in the process, earn interest.

How the Fed Sets Interest Rates

In the most simplistic terms, the Federal Reserve sets the federal funds rate.

This centrally managed rate, as we hinted previously, serves as an important, if

indirect, influence on other lending rates, which are otherwise governed by

normal market forces. If the Federal Reserve wants to reduce long-term treasury

interest rates, it might buy long-term treasuries on the open market. The

capital needed to purchase these treasures comes in the form of credit to the

banks which supplied the treasuries. This increase in available credit has the

effect of increasing the total amount of money in circulation.

During the financial crisis of 2007, the Federal Reserve also bought

mortgage-backed securities. This action helped bring mortgage rates down to a

level closer to the artificially lowered rates of treasuries.

In theory, the Federal Reserve operates this way because it can undo everything.

The Federal Reserve creates money and buys treasuries, but they can also sell

treasuries and destroy money. Though, in practice, the Federal Reserve has not

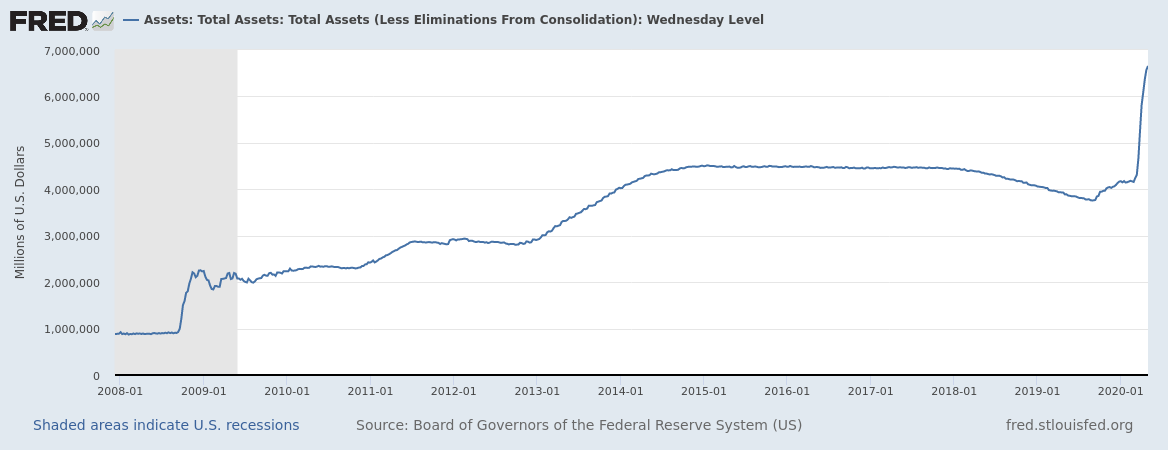

unwound purchases for over a decade. Below is a graph of the total amount of

assets that the federal reserve owns.

As illustrated, during the 2007/8 financial crisis, total assets rose quickly

from $1T to $2T, but then grew more slowly from $2T to $4T. Following this, we

see a bump after a small unwinding took place in lead up to the financial

markets becoming stressed. Unsurprisingly, a steep increase from $4T to $6.5T

occurred in response to the coronavirus, and I doubt it will stop there.

A New Asset For the Fed

Stress in the financial system was apparent in September of 2019. The response to COVID-19

has only made these stresses more visible and severe. Social distancing has

served to suppress economic activity for many companies. One concern is that

corporations might not be able to borrow and may be unable to service existing

loans. To avoid resulting bankruptcies, the Fed has set up two facilities that

will buy corporate loans.

Lending money to corporations involves some amount of risk. However, the Fed's

risk exposure is very different than to what a retail investor experiences. If a

company defaults on a bond purchased by the Federal Reserve, the Treasure

insures the exposure with money set aside for this purpose. This means that the

Fed can buy corporate bonds at effectively no risk.

Under normal operations, there is a beautiful dance that happens in credit

markets. Investors evaluate the risk vs. reward for particular bonds. If an

investor evaluates that the reward is worth the risk, the investor might decide

to purchase the bond. Each purchase by these investors will then slightly reduce

the value of that reward—from a broader market perspective.

Several motivations are at play when the Fed takes action. Purchases by the Fed

reduce the reward that corporate bonds offer without a corresponding evaluation

of the associated risk. Investors who understand this will most likely stay out

of the market. As general investors walk away, this puts pressure on the

markets to have the Federal Reserve step in and inject more cash. This scenario

effectively leads to a nationalization of the credit markets.

Counterthoughts

Some investment advice I try to keep in mind is, "invest in what you know." This

suggestion makes a lot of sense. How can you do better than other market actors

unless you have a better understanding of the fundamentals? So perhaps a take

away from this article is, if you were an expert in corporate bonds before,

maybe some outside analysis should be brought in to account for the actions of

the Fed. The market is a different animal now.

The fact is, all investments are relative, and markets are complex. The purchase

of bonds by the Federal Reserve may help keep businesses afloat. Maybe? In

that case, bonds will actually be worth more with Fed action than without. The

Fed's actions might raise the price of corporate bonds, but corporate bonds are

still better than other options for certain investors.

It is worth noting that the Fed's recent round of corporate bond buying is not

without precedent. The Bank of Japan has been buying corporate bonds for a

while now. Their economy failed to stabilize and now the Bank of Japan is

buying equities(stocks) outright.

The Bitcoin code includes a built-in mechanism to limit the total number of

bitcoins. Governed by algorithm, the protocol generates new bitcoins at a fixed

rate: a fixed number of coins every ~ten minutes 1. This implies a steady

increase in the coin supply. But there's a second half to that algorithm: every

four years, the per-ten-minute reward is halved. This ensures that the emission

rate of the coin eventually reduces to what becomes effectively zero. Since

this creation rate is halved each cycle, the event surrounding this reduction is

referred to as the halving.

The third such halving event will occur on or about May 12th. At that moment,

each new Bitcoin block will then include 6.25 newly mined (minted) bitcoins

compared to the 12.5 mined for each block now. Interestingly, this will be the

first time that Bitcoin's monetary inflation rate will be under the Federal

Reserve's 2% target for price inflation.

The History

Historically, Bitcoin halvings have been quite uneventful. I teach at the

collegiate level; I distinctly remember being between two classes when the first

halving occurred. As the event approached, I was engrossed, staring at my

computer screen, as I watched each new block being generated. The busy college

campus hummed along blithely unaware as first a block was generated with a 50

bitcoin reward, and then in the next moment, a 25 bitcoin reward. Blockchain.info

thoughtfully displayed some fireworks on the screen at precisely that historic

moment. Shortly thereafter, my students convened for their algebra class: not a

single mention, by anyone, of the event for which I was so excited.

From a technical standpoint, the whole flow of events was impressive. I was

impressed that humans could write a program that dictated the behavior of a

network years into the future.

The effect of the halving—and the corresponding supply reduction it

represents—to bitcoin's pricing, was difficult to discern in those first couple

four-year iterations. There were price spikes six months after each halving, but

whether there was a causal relationship, we simply don't know. A correlation

does not automatically imply a causal relationship.

Analysis

Here's the thought process I went through in November of 2012. I made the

following assumptions:

Bitcoin is a currency.

Demand for bitcoin is a constant.

Today, the first assumption is no longer valid as the number of transactions can

no longer support the currency use case. The second assumption I considered, at

least at the time, to be a conservative one. I measured the demand for bitcoins

as the amount of money it took to buy the newly mined coins—their value, in

fiat.

Long run

Given these assumptions, one would expect the price of bitcoin to double

eventually. This assumption had me hopeful about the future price of bitcoin.

But I wasn't happy with 'eventually.' I wanted to know just how quickly this

doubling would occur?

How Long is the Long Run?

In 2012, the price of one bitcoin was around $10. Therefore, for each 50

bitcoins generated, there was an associated $500 cost burden when they were sold

on the open market — $500 every ten minutes. After the halving, only $250 would

be needed to buy each new allotment of 25 bitcoins, leaving $250 of unmet demand

fed into the market cap. Or I at least assumed. $250 every 10 minutes comes to

$1.08 million per month. If this were factored into the market cap

algebraically, about 0.01 would be added to the price of bitcoin in the next

month.

So, with these assumptions, the price should eventually double, but it would

take a great deal of time. Using today's numbers, the time required to double

again would be even longer. Much longer.

Further Considerations

Note, even if the analysis found that the price would increase dramatically, the

psychological aspects of the bitcoin market may thwart the doubling at the

mathematically predicted time frame. When investors are alerted to a likely

rise in price, it stands to reason that rational actors would buy that item

before the expected price increase. This price pressure (sudden demand) would

then increase the price prematurely.

The Hype

On some social media, I commonly see mention of the halving in connection with a

price increase. Some quality tweeters have re-tweeted a stock-to-flow analysis applied to

bitcoin. But this analysis utilizes stock-to-flow concepts in a way I find to

be, frankly, underwhelming. They contend that one parameter, the stock-to-flow

ratio, determines the price of an item. A claim that, for me, seems to

oversimplify price expectations in this case.

This analysis considers three items: gold, silver, and bitcoin. The

stock-to-flow ratio of gold and silver are each measured for one point in time.

Those two data points are then used to make predictions about the price of

bitcoin over time.

Though, to be convincing, the author has much more work to do. At a minimum, I

would expect them to show how this stock-to-flow theory has successfully

determined the price of gold throughout its history. Specifically, how does

this ratio explain gold's rise from $300 in 1973 to $1,700 today? Additionally,

other failures of prediction for similar commodities—litecoin, for example—need

to be addressed.

Game theory is the study of one or more actors. The actors

engage in a competitive or collaborative activity. At the end

of the activity each actor has a way to judge the outcome and

compare the outcome to other outcomes.

Game theory applies to:

traders on the market

dating

mining cryptocurrency

Traditional games (chess, bridge, etc.)

as well as many other situations.

Not every player needs to be judged the same way. For an example,

consider Leslie who goes to the market and buys a peck of apples

from an apple farmer, Edna, for $4. Edna most likely valued

the apples sold at less than $4. As Edna has

lots of apples and would like to sell them before they rot.

Leslie wanted the apples so much she not only parted with $4 but

decided to use her time to seek out apples.

In game theory the value that each actor puts on each outcome is

called a utility function. In our example Leslie might find

the utility of laving the market with a peck of apples to be more

than the Edna, who has apples at home. Utility is intended

to be a measure of the value, or the enjoyment, or the use of an

item or situation.

Utility could be a subjective concept, but is useful when comparisons

can be made.

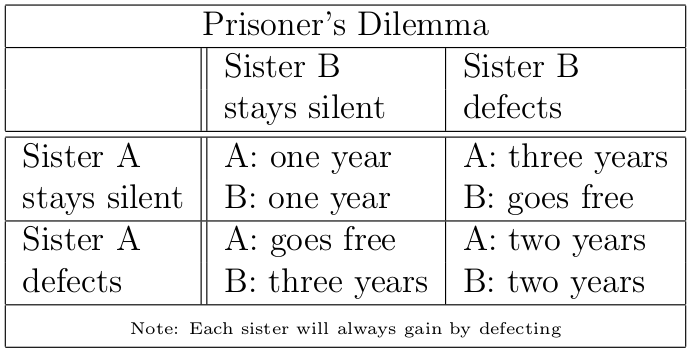

In game theory there is a very famous example of a game known as the

prisoner's dilemma. This situation happens when two sisters rob an

electronics store. The police find each one of them driving a van

full of stolen big screen TVs. Each of the sisters is arrested and

taken in for questioning without the opportunity to talk to the other

sister. The police then give each sister a choice. The choice is

to tell on their sister and receive a year off any prison sentence.

As it stands, each sister is facing a year of jail time for possessing

the stolen televisions. The table below explains the consequences of

the sister's option to stay silent or defect from her family.

Now, basically the best outcome for both sisters for each of them

to stay silent. That's the outcome that has the least amount of total

jail time. However this outcome is unstable. In the case that

both sisters stay quiet either one will gain (go free) from defecting.

And even if one sister defects the situation is still unstable as the

other sister could serve two years instead of three by telling. In

fact each sister is always better off by defecting, no matter what

the other one does. If both sisters do defect then neither sister

can improve their outcome by their choice alone.

This game provides some insight into why, in some cases, corporative

solutions are never sought after.

A Modest Proposal of Some Bitcoin Cash Miners

A proposal of Jiang Zhuoer and signed by other miners has been made to the

Bitcoin Cash community. This proposal encourages

other miners to orphan blocks that do not provide for a fund for

developers. The proposal has a clear begin date and end date.

The proposal claims that it is not a change in the protocol. However,

it would be a change in "a set of conventions governing the treatment

of data in an electronic communication system." Which is a change

in protocol according to Merriam-Webster. I think the author of the

proposal meant that this proposed change in protocol would not

be hard coded in the client.

It is the very fact that this protocol change is not hardcoded

allows for this game theoretic analysis. We hope to understand the

game theoretic implications of this type of protocol change.

Miner Behavior

Clearly there is anecdotal evidence that some people support

funding developers in the form of the proposal. There is also

anecdotal evidence here and here that some

people don't support the proposal.

Even better, is the fact that SHA256 mining allocation is very well

understood and

miners generally go after the most profit. cite: Bissias, Levine, Thibodeau.

For our game theoretic analysis we assume that 30% of the miners

are ideologically driven in favor of the proposal.

They assign a high utility to all blocks funding developers.

The exact amount of value they assign the dev fund does not effect

this analysis. The people who support the dev fund expect

that this fund will pay off in the future in the form of a higher

price. Economists would say that people that support the proposal

have a low time preference. Also miners that support the proposal

have a higher risk tolerance, as the dev fund is, in effect,

investing in a startup. As we understand miners risk tolarance to

be quite low (Bissias, Levine, Thibodeau) we expect that 30% is an overestimate.

We assume that all other miners are maximizing (revenue and therefore) profit.

The Game

If the 70% of miners that are profit maximizing know that they

will all act together, then they can sleep easy knowing that

following the longest chain and ignoring dev funding will

maximize their profit.

However, just like the electronics thief sister being questioned,

the miners don't know if their sister miners will defect to the

other side or not. As we will see, one major advantage is that

the miners can coordinate their action. They can talk to each

other.

As simplifying assumptions we assume that the 30% in favor of

the dev plan always mine a chain consistent with the dev

funding. To explain

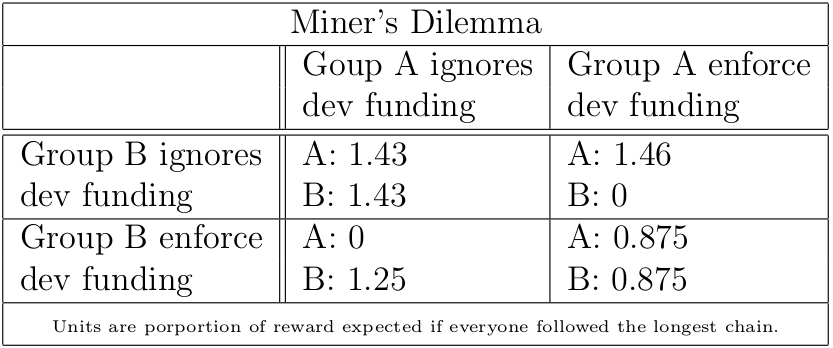

the incentives we break the profit seekers down into group A

which is 30% of the hashing power and group B which is 40% of

the hashing power. In such a case we have

From this table we can see that if 30% (and not less than 20%) of

the profit seeking miners

enforce dev funding they will profit more. However, if 40% of the

miners enforce dev funding then they will all collectively loose.

However, if the longest chain is enforcing the dev funding then

it's in everyone's interest to switch.

This analysis ignores the fact that BCH is a minority chain.

Considering this fact, it's likely that hashing power would be

attracted or repelled from BCH to balance out the profitability.

This is asserted in the dev funding proposal, and to a very

good approximation is correct.

The Sisters Talk

We're talking about miners on a public blockchain. They are not

being held incommunicado like our sisters above. Mining

participants could advertise the protocol they follow in

the version number of a block that they mine.

This could go both ways.

Miners like Jiang Zhuoer that want to fund the developers could

flip a bit in their version number and if a sufficient number

of blocks signal for the protocol rule at the scheduled MTP then

dev funding could be safely enforced.

It works the other way as well. Miners that want to follow the

longest chain could signal that with a

bit in the version number. As long as a sufficient number of

miners signal they are mining the longest chain then miners

can safely add to the longest chain.

There is the opportunity that miners could lie. However,

most of the time, lying in this circumstance does not help your

cause. For more information about using the version number to

signal the desired protocol to mine see BIP0009.

Conclusions

Having a consensus rule that is not enforced by the nodes

leads to some very interesting game theory. If the consensus

rule is enforced by all nodes than it would be in every

miners interest to enforce the rule on that chain. However,

if the consensus rule is controversial then there is a

serious risk of forking off yet another minority chain.

Perhaps the best that can be hoped for is that both sides

agree on one bit of the version number. Then use that bit to

signal if funding for developers is enforced or not. As long as

both sides can accept the results of the miner's vote then

then the current Bitcoin Cash network does not risk a split.

To be clear, using a version bit to signal which protocol to

follow may result in a genuine compromise. That is, a

situation where the dev fund is only funded some

of the six months that is asked for.

To me using a bit in the version is the polite way to mediate

this dispute.

Last Friday I was interviewed by Dash News, We covered topics relating to

chainlocks and their security. We also talked about reducing proof of work

for Dash. We discuss how SPV wallets could take advantage of chain locks to

provide more security even with less work in every block.

We talked about the economics research going on right now at ASU. That

is the part of research that I am involved in and most excited about. We talk

about a lot of options. The hosts relate these decisions to being a central

bank, and there is a parallel that can be drawn. Perhaps I didn't get across

that the goal is to have a hands off economic policy. My hope is that

a stable economic model can be adopted and hardcoded without intervention

after the change. I

lament that we did not talk about the Zero Knowledge Proof research also being

worked on by the ASU blockchain research lab. I expect an update on that by

the end of the school year.

I was asked about Dash's monetary inflation. It was purported that Dash's

monetary inflation was high, and it is compared to other cryptocurrency projects.

I'm hoping that any changes to the inflation schedule result in less issued Dash.

There is some discussion about masternode voting participation. Now that

voting keys are on chain then it would be nice if a phone app allowed for

voting on your phone. I think that would encourage more voting. Mark suggested

that TAPPMATH could explain the calculations in the chainlocks security analysis in

more detail.

If you haven't had a chance to watch this episode please find a video of it below.

Darren Tapp

Darren Tapp